On rare occasion does the Federal Reserve cite international developments as a major factor in its domestic policy decisions, but that is precisely what happened this September. Despite a strengthening U.S. labor market and an increase in the Fed’s own projection for U.S. growth next year, the Fed decided to delay its much anticipated lift-off of its key policy rate from about zero. The Fed’s two objectives of price stability (inflation at the Fed’s desired rate of 2 percent) and maximum employment are domestic ones, yet its decision this September was based on the impacts of “global economic and financial developments” on those objectives.

These developments – a weaker world economy, stronger dollar and lower energy prices – are serving to keep inflation subdued longer than expected. As global factors are pushing inflation down for the time being, the Fed has opted to delay the gradual process of increasing its key policy rate until it is more confident that domestic factors are in a better position to help push inflation higher – namely, a stronger labor market.

A Diverging World

In anticipation of a rate rise this year in a strengthening U.S. economy, capital outflows began to accelerate from many emerging markets, adding pressures on their already slowing economies. Declining oil and commodity prices were already hurting many commodity exporting countries like Brazil, and those prices remain lower as global demand remains weak. Concerns began to grow over a faster than expected slowdown in China and the ability of the Chinese authorities to manage that slowdown. These concerns manifested themselves through significant financial market volatility and further downward pressure on emerging market currencies, elevating the downside risks to not just the outlook in developing countries but globally as well.

Adding to financial market jitters and depreciated emerging market currencies is the adjustment to the divergence in policy among the world’s major central banks. The Fed and the Bank of England are slowing down their accommodative stances (ended QE and will be raising rates), while the European Central Bank and the Bank of Japan are expanding their accommodation through their own quantitative easing programs.

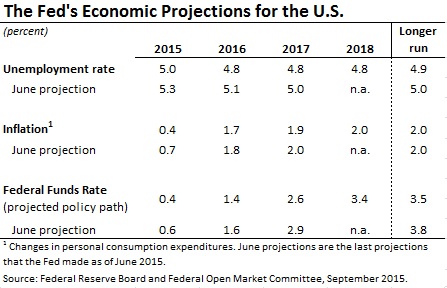

Meanwhile in the U.S., the outlook looks much brighter. Overall growth in the first half of 2015 was faster than expected at 2.25 percent, continued job gains and increases in household income have supported spending and the unemployment rate continued to decline closer to its longer-term normal level. According to the president of the San Francisco Fed, the U.S. should reach full employment on a broad set of measures by the end of 2015 or early 2016. At the same time, the Fed’s other objective – 2 percent inflation – remains well below its target as energy and import prices remain low.

Against this backdrop of a weaker global economy and a strengthening U.S. economy where the Fed is getting closer to one of its objectives but not the other, the Fed made the assessment that these global factors were delaying progress on its inflation objective.

With interest rates at zero, the Fed cannot lower them any further. This would make it harder to react to any more bad news. On the other hand, if growth and inflation suddenly pick up, the Fed can raise rates to manage a more controlled rebound. The arguments for waiting to raise interest rates highlight this asymmetry in the Fed’s ability to react to changing economic circumstances. The concern that further global developments can get in the way of the Fed’s objectives is made evident by recent financial turmoil in China along with the economic and policy conditions abroad – weak foreign demand, cheap commodity prices, QE in Europe – that have contributed to a stronger dollar, holding back U.S. growth and inflation.

Unemployment and Inflation

Though the Fed believes the pressures on inflation from abroad will subside over time, it decided to wait

Though the Fed believes the pressures on inflation from abroad will subside over time, it decided to wait

for another source of inflation – a stronger labor market – before raising rates.

The relationship between unemployment and inflation is a classic one in macroeconomics. The idea is that lower unemployment eventually leads to higher inflation as employers increase wages and then raise prices to make up for the added cost. The “non-accelerating inflation rate of unemployment”, or NAIRU, is the estimated unemployment rate at which inflation does not speed up or slow down. Any unemployment rate below NAIRU is expected to push inflation higher. Since 2013, the Fed’s estimate of NAIRU has been declining slowly and a bit faster over recent months. This suggests that the Fed believes unemployment needs to move lower and lower before it can have a positive impact on inflation.

With global factors pushing inflation down not just in the U.S. but around the world, the Fed will need a tighter domestic labor market to help meet its 2 percent inflation goal. In fact, the Fed projects the unemployment rate to dip slightly below its longer run level over the next couple years as inflation moves closer to 2 percent. If the bad news abroad keeps up, the stronger the labor market may need to be to justify a rate rise.

The Path Ahead

The timing of the initial lift-off in interest rates remains a delicate matter. The Fed does not want to wait too long and risk overshooting, where inflation could increase above the 2 percent target. In that case, the path of the increases in the federal funds rate towards its longer-term normal level (which now may be lower than before the crisis) may be too fast and too steep, hurting overall economic growth.

Monetary policy operates with a lag, meaning it takes time for a change in interest rates to trickle through the economy. If the Fed waits until inflation is already close to its objective before raising rates, it runs the risk of having inflation overshoot its target.

On other hand, if the Fed acts too soon, it risks derailing economic momentum and progress towards its objectives. This would force it to bring rates back down and find itself in a less credible position. This is what happened with the European Central Bank and the Swedish Riksbank in 2011.

The majority of the members in the Fed’s interest-rate setting committee believe that the appropriate time to raise rates likely remains in 2015. They could agree to begin raising rates after their next meetings in October and December if they see in the data a stronger labor market and perhaps a somewhat calmer global environment. Otherwise, they have left the option open to delay this process even further. Once lift off occurs, the Fed has been clear that it will follow a gradual path for the federal funds rate to reach its longer run level and that overall Fed policy will remain accommodative for some time.

The majority of the members in the Fed’s interest-rate setting committee believe that the appropriate time to raise rates likely remains in 2015. They could agree to begin raising rates after their next meetings in October and December if they see in the data a stronger labor market and perhaps a somewhat calmer global environment. Otherwise, they have left the option open to delay this process even further. Once lift off occurs, the Fed has been clear that it will follow a gradual path for the federal funds rate to reach its longer run level and that overall Fed policy will remain accommodative for some time.

Going forward, the Fed will need to communicate clearly so that reactions to its policy actions won’t be too disruptive in the U.S. and abroad. In emerging markets, uncertainty around when the Fed will act is partly contributing to financial market and exchange rate volatility. The central bank governors of Mexico, Peru, India and the deputy governor in Indonesia have all expressed their preference for the Fed to raise rates to end the uncertainty that is unsettling financial markets and posing risks to their economies.

Ultimately, economies around the world will have to adjust their own policies with a focus on making their economies more resilient to global events. Even though the Fed takes the rest of the world into account, its goals lie inside the United States.

This article is available in Spanish at La Grieta.

BACKGROUND

Fed Policy since the Financial Crisis: For the last six years, the Federal Reserve has kept its key policy rate, the federal funds rate, between 0 and 0.25 percent in support of a U.S. economic recovery after the global financial crisis. This historically low interest rate, however, was not enough on its own to help kick-start economic activity after the crisis. The Fed had to resort to a more direct, and unconventional, method of pumping money into the system. Since low borrowing costs were not encouraging money to flow through the economy after such a severe crisis, the Fed stepped in “quantitatively” by directly buying bonds and moving a significant amount of debt from the private sector onto its own balance sheet – hence “quantitative easing”. Five years and $3.5 trillion later, the Fed ended QE but continued to hold on to the debt it assumed and kept its key policy rate at zero to continue to accommodate a strengthening yet still recovering U.S. economy. The Fed announced that 2015 would likely be an appropriate time to begin to gradually lift the federal funds rate from the ‘zero lower bound’.

The Relevance of Interest Rates: The federal funds rate is the rate at which banks charge each other for overnight loans, which they may need in order to make sure they have enough reserves parked at the Fed (a requirement). This short-term interest rate ripples through the economy to affect rates on mortgages, auto loans, student loans, credit cards, and the general cost of borrowing. It also affects the exchange rate and thus the cost of exports and imports. A higher interest rate is meant to keep the economy from overheating (when prices begin to rise too fast and borrowing becomes excessive) by discouraging borrowing and encouraging saving. A lower interest rate is meant to stimulate a slow economy by encouraging lending and economic activity through lower borrowing costs. In a global economy, money flows to where it can achieve a decent return. If a country’s interest rate increases, it attracts more money from overseas, strengthening its exchange rate. A stronger currency makes the prices of imports cheaper at home while making exports more expensive to foreigners abroad, widening the trade balance.

See Inflation: Slowly Rising Prices Can Be a Bad Thing to understand how low inflation can be bad for economic growth.

See The Global Economy Can Hold The US Back to understand how a weak global economy can undermine a strengthening US economy.

RELATED MATERIALS

Federal Reserve issues FOMC statement, 17 September 2015.

FOMC: Press Conference with Fed Chair Janet Yellen, 17 September 2015.

Federal Reserve Board and Federal Open Market Committee release economic projections, 17 September 2015.

President of the San Francisco Fed: China, Rates, and the Outlook: May the (Economic) Force Be with You, 19 September 2015.

Backgrounder from the IMF: Monetary Policy: Stabilizing Prices and Output.