This is the third post in a series on how a weaker global economy can threaten the strengthening recovery in the US. The first post in the series is the introduction, which is followed by three parts. Part I, delves into the drivers of growth in the US and in the rest of the world. This post, Part II, explains the basics of an open economy and analyzes the recent rise of the US dollar and the role of the trade balance in the US economy. Part III ties it all together by discussing the importance of demand to the US and global economies.

In this part we discuss the basics of an open economy and the importance of exports and the trade balance to the US economy. Although the main driver of growth in the US is consumption demand, exports have been playing an increasingly important role since the financial crisis. The dollar is central to US exports and imports, and a rising dollar, although reflective of a strong US economy, can hurt US export competitiveness and shift US consumer demand overseas.

If you understand well the concept that exports add to and imports subtract from GDP, and are familiar with what an exchange rate is and what makes it stronger or weaker, then you can skip the first section and proceed to the following one on the dollar and the US trade balance.

The Basics of an Open Economy

To better understand how a weak global economy can affect a single national economy, one must look at the channels in which an economy links with other economies beyond its border – international trade and finance.

The overall GDP of an economy can be measured as the sum of consumption, investment, government spending, and the trade balance (exports minus imports). Rephrasing that sentence into a simple and well known equation, we have: GDP = Cons. + Inv. + Gov. + (Exports-Imports). Note that exports contribute positively to GDP, while imports subtract from GDP. This is because exports reflect demand (albeit from abroad) for national goods made and sold by firms inside the country. Imports are the opposite, and reflect consumers sending their money abroad to buy foreign products, benefitting incomes in foreign countries.

Note that this does not necessarily mean that exports are always good and imports are bad. Countries engage in trade with each other because it benefits them – some in supplying goods because they can produce more efficiently or because domestic demand is not fully developed, and others in demanding them because they have the income (or credit) and the need.

If the trade balance becomes too large, however, significant risks can emerge. If a trade deficit, for example, is largely financed through credit (borrowing money to buy imports) and becomes too large relative to GDP, then the associated risks of too much debt for households and firms can spread across borders and effect more economies. This is because the money sent abroad is borrowed money, often resulting in cross-border liabilities. The Financial Times has a great animation explaining why trade balances matter.

When buying and selling products internationally, then payments must also be sent and received internationally. This requires at least one party in the transaction to exchange its currency to the currency of its trading partner in order to pay for the product. This is where the exchange rate comes in – how much one currency is worth in terms of another currency. If one currency, say the British pound, is worth a lot in terms of another currency, say the Chinese yuan, then a single pound can go a long way in buying Chinese products whose prices are set in yuan.

A final amount paid in pounds for a Chinese import is then based on the price in yuan and the exchange rate used by the British buyer to convert her currency into yuan. This is why both prices and exchange rates are important for export competitiveness (in this example, the Chinese are the exporters).

Like the price of any normal product, the price of a currency (the exchange rate) increases when demand for that currency increases. Demand for a currency can rise for two fundamental reasons: interest rates on government bonds rise (higher returns) and higher growth and investment prospects (via stock markets or foreign direct investment). People abroad would want to send their money to another country to buy their products or invest if that country can offer higher or more stable returns.

In the US today, government interest rates are not rising but are higher and considered safer than in other developed countries. Growth, though, is rising and getting stronger, as established in Part I. This is a big reason for the rise in the dollar and is where demand comes in.

In general, rising consumer demand applies to both domestic and imported goods. As more disposable income is available to consumers, part of that increase will go to imported products (economists call this the marginal propensity to import).

With that in mind, a strengthening US economy and a weakening global economy are most clearly reflected in the recent rise of the US dollar and the widening US trade balance.

The Dollar and the US Trade Balance

In mid-April 2014, after a few consecutive months of strong job creation and around the time when stronger GDP growth was beginning to gather momentum, the dollar began its consistent and relatively rapid rise. Since then, the dollar has increased consistently by over 10 percent relative to a broad basket of currencies (17 percent against major currencies), bringing it back to where it was in the wake of the Lehman collapse in 2008.

A dollar in demand is typically welcome news for the US. It reflects strengthening economic prospects as described above and increasing investor attention to the US market. It also reflects weakness and lack of sustained growth in other parts of the world, further encouraging investor demand for US assets. Higher interest rates in the US (though still historically low) than in other developed markets and expectations for the Federal Reserve to raise interest rates sooner than later also support the chances that the US dollar could continue its rise (this relationship is explained above).

Indeed, divergent economic performance between the US and the rest of the world encourages the rise of the dollar which could hurt US export competitiveness. The two are interrelated, as weak external demand (demand for US products abroad) is made weaker the stronger the dollar gets (as products priced in dollars become more expensive in other currencies).

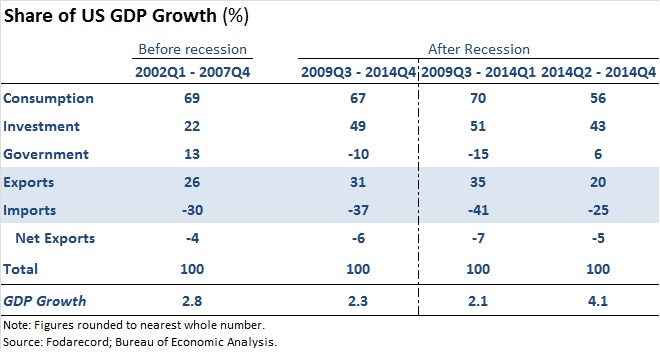

Some countries are more reliant on exports for growth than others. In the US, consumption demand is the largest component of GDP and contributor to GDP growth. US Exports, up 17 percent since the pre-recession, have increased in importance, however. Imports are up 4 percent from their pre-recession peak. Exports have accounted for 13 percent of GDP, yet over 30 percent of GDP growth since the recession officially ended in the third quarter of 2009. This is in comparison to a 10 percent share of GDP before the recession and 26 percent share of GDP growth.

Separating out the last three quarters of 2014, when the dollar began and continued its surge, exports had accounted for 35 percent of growth before dropping to 20 percent. Though the US oil boom drove its trade balance to a four year low in late 2013, the trade deficit rose in 2014 by 6 percent despite a 55 percent drop in the price of oil that year.

The recent rise in the US trade balance last year is a result of both a 2.9 percent drop in exports and a 3.4 percent rise in imports. This could suggest that both the rising dollar and rising US consumer demand are at play through declining export competitiveness and weak external demand on the export side, and stronger purchasing power for a resurgent US consumer on the import side. Weakness in the rest of the global economy would fuel this, and that appears to be the case with the US’s largest trading partners outside of North America – the euro area and China.

The euro area is the US’s largest export market outside of North America, and third largest source of imports behind China and neighboring Canada. Weak demand is therefore a concern for US exports, and the euro area as a whole is running a current account surplus of close to 3 percent, with countries like Germany running its largest trade surplus at 7.4 percent of its GDP, thanks largely to exports to the US. Countries with surpluses imply that they benefit from demand from other countries more than demand within their own borders.

The euro has fallen 17 percent against the dollar since early last year, and the ECB’s quantitative easing program suggest that despite any hopeful uptick in demand in the euro area, the euro is likely to remain weak vis-à-vis the dollar relative to its past.

China, the US’s second largest export market outside of North America and overall largest source of imports, is the largest driver of the US trade deficit. From 2010 to 2013, the renminbi (China’s currency, officially the yuan) has been allowed by China’s central bank, which has controls over the value of the renminbi, to appreciate 10 percent against the dollar. Amidst the troubles in the Chinese economy that were mentioned in Part I, China has arguably “allowed” the renminbi to depreciate again and fall 3 percent against the dollar last year. Though exports and imports have declined in China and the renminbi remains stronger vis-à-vis the dollar compared to 2013 when it started to depreciate again, it will be important to see what extent the Chinese increasingly look towards external demand as a source of growth again. In that scenario, the US, with its rising trade deficit, could be directly affected.

With increasing pressure on a growing US trade deficit, consumer demand in the US could be increasingly sought after if other parts of the world fail to stimulate their own demand. A stronger US dollar would only encourage the pressure on the trade deficit to widen even further. We have now seen how a rising dollar impacts the trade balance through declining exports and rising imports. In Part III, we tie it all together by focusing on the import side of the trade balance and the global quest for badly needed consumer demand.

Introduction: The Global Economy Can Hold the US Back

Part I: A Stronger US in a Weaker Global Economy

Part II: The Rise of the Dollar and the US Trade Balance

Part III: The Quest for Demand and the US Consumer

[…] The Relevance of Interest Rates: The federal funds rate is the rate at which banks charge each other for overnight loans, which they may need in order to make sure they have enough reserves parked at the Fed (a requirement). This short-term interest rate ripples through the economy to affect rates on mortgages, auto loans, student loans, credit cards, and the general cost of borrowing. It also affects the exchange rate and thus the cost of exports and imports. A higher interest rate is meant to keep the economy from overheating (when prices begin to rise too fast and borrowing becomes excessive) by discouraging borrowing and encouraging saving. A lower interest rate is meant to stimulate a slow economy by encouraging lending and economic activity through lower borrowing costs. In a global economy, money flows to where it can achieve a decent return. If a country’s interest rate increases, it attracts more money from overseas, strengthening its exchange rate. A stronger currency makes the prices of imports cheaper at home while making exports more expensive to foreigners abroad, widening the trade balance. […]