This is the second post in a series on how a weaker global economy can threaten the strengthening recovery in the US. The first post in the series is the introduction, which is followed by three parts. This post, Part I, delves into the drivers of growth in the US and in the rest of the world. Part II explains the basics of an open economy and analyzes the recent rise of the US dollar and the role of the trade balance in the US economy. Part III ties it all together by discussing the importance of demand to the US and global economies.

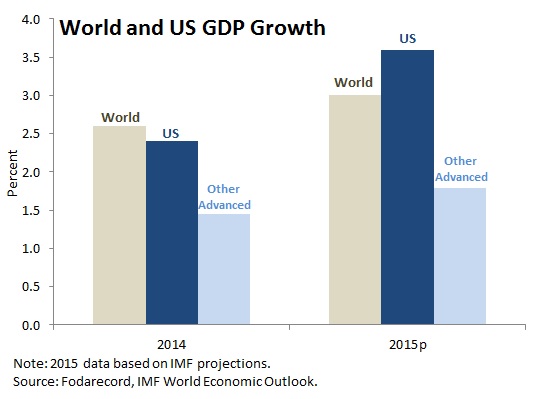

This year is a crucial one for the global economy. It will need to balance the positive economic forces encouraging a stronger global recovery with the headwinds that can drive divergent paths among major economies. There is a real opportunity given low oil prices and low interest rates for investment, but that may not be enough to offset the negative factors. The IMF just lowered its growth projections for every major economy except for the United States, which is now projected to grow faster than previously expected. Let’s take a look at how the US is doing well and how most others are not doing as well.

The US

Since the second quarter of 2014, GDP growth in the US has been stronger than any other comparable period since 2004.[1] Although the most recent quarter came in below expectations for GDP, consumer spending (which is 70 percent of US GDP) was the strongest since 2006. Low energy prices have certainly helped, with spending on gas for US households on track to be the lowest since 2003. Consumer confidence, as measured by the University of Michigan, is at its highest level since 2004.

Central to the US story is the rebound in the labor market. The once “jobless recovery” in the US has now created an average of 267 thousand jobs a month over the last twelve months. This is a much stronger pace than the 170 thousand jobs a month created prior to then and since 2010 when the US began its longest ever period of uninterrupted job creation.

Central to the US story is the rebound in the labor market. The once “jobless recovery” in the US has now created an average of 267 thousand jobs a month over the last twelve months. This is a much stronger pace than the 170 thousand jobs a month created prior to then and since 2010 when the US began its longest ever period of uninterrupted job creation.

In 2014, more jobs were created (over 3 million) than in any year since 1999. Also in 2014, the decline in the long-term unemployed was the largest since the crisis, now 60 percent below its peak in 2009 although still at a historically high level. Though the unemployment rate last month inched up to 5.7 percent despite strong job creation, it was primarily due to a rise in the number of people looking for work. Wage growth has shown early signs of gains, but it is still too early to tell if it will remain strong enough for long enough. In fact, stagnant wages have plagued the US economy for decades and are perhaps its biggest and most significant challenge to its long-term health.

The risks in the US remain significant, however.

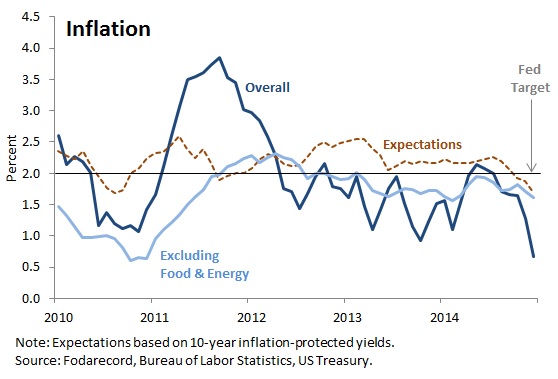

Aside from the jury still being out on whether wage growth will continue, low and declining inflation remain a key challenge for the US economy. The inflation rate remains below the Federal Reserve’s target of 2 percent and is headed lower along with expectations of future inflation. As discussed previously on the Record, low inflation can be problematic because it places downward pressure on both consumption and investment. Part of the decline in overall inflation can be attributed to falling oil and energy prices, yet core inflation, which excludes food and energy, is also declining further below the Fed’s target. A strengthening labor market and rising consumer spending should bode well for the inflation outlook, but as of now it is not reflected in the data. Rising consumer spending without consistent wage growth, however, could signal risks of a return to credit-driven (borrowed-money-driven) spending, reminiscent of the years that led up to the global financial crisis. This is discussed further in Part II.

Also discussed further in Part II is the rising US dollar which best reflects the divergent paths the US and the rest of the world are on in terms of growth and demand. The more the rest of the world looks to the US alone to drive growth, the stronger the pressure on US momentum and on the dollar, which in turn could add further pressure on momentum. Part II delves into the links between the US and the broader global economy, which include international trade, finance, and the exchange rate.

The World

Perhaps the biggest boost to global growth prospects is the drop in oil prices that began in mid-2014 and lasted until the end of January. The IMF estimated that this boost could add anywhere from 0.4 to 0.7 percent to global GDP growth (with the benefit even stronger in most advanced economies), yet at the same time revised down its projections for global growth this year. Citing lower investment, market volatility, stagnation in Europe and Japan, and geopolitical tensions, the negatives could outweigh the positives.

The euro area has grown at a meager 0.2 percent in the first three quarters of 2014, and the threat of deflation has turned into a reality. On the positive side, lower oil prices provide some relief and the European Central Bank (ECB) has begun its long anticipated quantitative easing (QE) program in an effort to lift inflation and support demand. Although investors were at first unconvinced, inflation expectations in parts of the euro area – Germany and Italy – have picked up in the last two weeks as a reaction to QE. Nevertheless, current prices are still declining, output is shrinking, tensions between Ukraine and Russia are flaring right by the euro area’s border, and the disagreements between Greece and Germany (through the European Commission), the ECB, and the IMF are raising the concerns over a destabilizing Greek exit from the union.

Japan fell into recession in the third quarter of 2014 and has now delayed the second increase in a new consumption tax that was introduced in the second quarter of 2014. Additional stimulus from the Bank of Japan and a depreciating yen should give the Japanese economy some relief.

In China, the world’s second largest economy, an adjustment to a “new normal” of relatively slower growth is underway. Although slower growth from a higher GDP level is not by itself a cause for concern, the financial and economic risks that have been brewing in China are causes for concern for itself and its trading partners. Increasing vulnerabilities from rapid credit-fueled investment growth are taking their toll on growth in China, inhibiting the desired shift from an investment-led to a consumer-led model for growth. After decades of very high investment rates, there is an over-capacity and excess supply in China that is creating problems for its financial sector and will require the attention of its authorities and impact its growth. Some argue that it is actually China alone that has been the cause of the global economy performing below where it could be.

In other emerging and developing economies, geopolitical tensions and the drop in oil and other commodity prices will contribute to a drag on growth. Russia, an economy heavily dependent on oil (see Russia, Left in the Ruble), is suffering from the drop in oil prices. Its central bank had to step in to fight a currency crisis and its economy is expected to shrink rapidly this year. Other oil exporters are also negatively affected by oil prices, and only some (notably in the Gulf) can avoid big cuts in government spending to compensate for lower oil revenues. Drops in other commodity prices, encouraged in part by the slowdown in China, have affected commodity-exporters in general, notably those in Latin America.

Spilling Over Into the US

It is clear that the US is the one bright spot in a dim global economy. Though the US is the largest economy in the world at 22 percent of global GDP, it cannot continue to approach its potential as rapidly as it could without a relatively healthy global economy. US Treasury Secretary Jacob Lew has said that the US is entering a period of “self-sustaining” growth, but acknowledged that the US “cannot do it alone.” Part II establishes the link between the US economy and the global economy and the instruments that facilitate this link, namely the US dollar.

Introduction: The Global Economy Can Hold the US Back

Part I: A Stronger US in a Weaker Global Economy

Part II: The Rise of the Dollar and the US Trade Balance

Part III: The Quest for Demand and the US Consumer

[1] Based on the average of annualized quarterly growth rates, growth in the US over this period (2014Q2-2014Q4) was 4.1 percent.