For the first time in history, the largest economy in the world will be poor. Last week, the World Bank revealed that prices in developing countries are much lower than we previously thought, implying that the purchasing power of citizens in those countries is stronger. Taking this into account, new estimates of GDP at purchasing power parity (PPP) show that China’s economy will be larger than the US’s by the end of this year. However, this new result can be misleading. When looking at the total size of an economy, it is regular market prices that are most useful, not PPP prices. What the new PPP data tell us is that standards of living in developing countries are higher. Although China’s standard of living has improved, it still ranks 99th in the world in income per person, just behind Egypt.

Real GDP Per Capita vs. Population, 2011

In the future, China’s economy will become the largest in the world in both market and PPP prices. With a population of 1.34 billion people, however, it will take much longer for China to become a rich nation. Today, its weight and influence in the global economy is still a function of its size at standard market prices.

Taking a step back, the PPP-versus-market prices debate is a common one in international economics. Since different countries use different currencies, comparing economies requires converting their respective currencies into a common one using an exchange rate. The market exchange rate is the price of one currency in terms of another.

When a person wants to purchase a good or service priced in a different currency, he or she must use the market exchange rate to convert one currency into the other. These goods and services that cross international borders comprise the tradable sector, and the prices of these goods are similar across countries (minus taxes, customs, shipping costs, etc.).

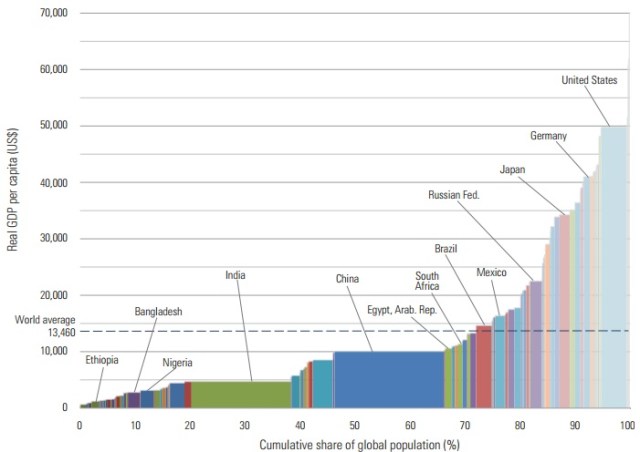

Prices found in the non-tradable sector (local goods or services that cannot be traded like haircuts and plumbing, e.g.) are what vary across countries, especially between rich and poor. If two households in two different countries have identical incomes but prices are lower in one country, then the household in the country with lower prices will have a stronger purchasing power and thus a higher standard of living. PPP exchange rates account for this, and are therefore more useful when comparing GDP (income) per capita and standards of living.

Since PPP measures are used to compare standards of living, they therefore also tell us something about global poverty. According to initial estimates by my colleagues at the Brookings Institution, the new data reveal that the number of people in the world living in extreme poverty is 340 million less than previously estimated in 2005. That is about the size of the U.S. population.

Although PPP is better suited to compare income per capita, comparing national incomes at market exchange rates are what matter for global commerce and global influence. As discussed by Jeffrey Frankel and by Martin Wolf, China’s trading partners look at the size of the Chinese market at prevailing market prices, which show that China’s gross imports are still 31% smaller than the US’s. Despite China’s efforts to internationalize its currency, the renminbi, there is no serious challenge to the role of the dollar as the global reserve currency. In fact, China itself holds the majority of its $4 trillion of reserves in dollars. Other measures of global influence, such as purchases and sales of military equipment or voting power in multilateral organizations like the IMF, are assessed under market rates. Comparing the size of national economies as an indicator of a country’s level of influence in the world is therefore better done under market prices.

Though the PPP numbers suggest that China will overtake the US, China is still about 55% the size of the US in current market prices. Eswar Prasad further elaborates on the limited challenge China currently poses to US leadership in the world.

However, PPP data can tell us something about market exchange rates. In economics, the Balassa-Samuelson effect shows that the lower the GDP per capita of a country, the lower the prices of non-tradables should be in that country. Lower prices for non-tradables free up more purchasing power for goods in the tradable sector. If prices are below what they should be according to the Balassa-Samuelson effect, then the exchange rate is depreciated. Martin Kessler and Arvind Subramanian use GDP per capita at PPP prices to test this relationship. For 2005 prices and income, they found that the renminbi was about 30% undervalued, as is commonly claimed by US politicians and media. Using this same approach with the new data released last week, Kessler and Subramian found that as of 2011, the renminbi was only 1.7% undervalued. Since 2011, the renminbi appreciated faster than the Balassa-Samuelson would have predicted (given income per capita growth in China over that time), suggesting that the 1.7% undervaluation in 2011 has been effectively undone and the renminbi is fairly valued – a finding that China’s competitors may be reluctant to believe.

Of course, there are many different methods to estimate the true value of a currency, but these results use the same approach that previously suggested a large undervaluation. Gavyn Davis at the Financial Times provides some insightful analysis on what the new PPP numbers say about China’s changing exchange rate policy.

The new PPP estimates are the result of the most extensive effort to measure purchasing power parities ever. Though concerns have been raised about the data, they are the most accurate and best source for PPP’s available, and a big improvement in methodology from previous estimates.

Interpreting the data, of course, is always the most powerful use of it. The finding that China will overtake the United States in aggregate GDP is not true under market prices, and is not meaningful under PPP prices. The PPP data do tell us that standards of living in developing countries are higher than previously thought. Given its large size and that it is expected to continue to grow faster than the US, China will soon be bigger than the US in both market and PPP terms, but it will be much longer time for it have the same level of influence in the world.